How can you catch up with Challenger Banks? What can you do to become a disruptor? Is investing in technology the only effective solution? These kinds of questions deepened the minds of more than 100 participants of the EFMA Asian Retail Banking Summit 2019, which took place on 6-7.11.2019 in Singapore. During these two intensive days, we could hear the answers to these and other questions. They were provided by the representatives of Asian banks and companies supporting them in their development. Following our summary of the EFMA Innovation Summit in Paris, we will try to present below the main topics that were discussed during the Singapore conference.

Transformation to new banking models

Many of the presentations that we could see and hear touched upon different banking concepts seen from the perspective of different countries. These concepts related not only to a new opening for traditional banking with branches but also to a mobile-only approach to banking. What connects these concepts are certain groups of banks from many countries that, either on a local or global scale, are challengers. Or disrupters. These leaders on the banking market know how to combine innovation, technology, UX, and being accessible for each client, as mentioned by Manohar Chadalavada from Standard Chartered Bank.

A similar opinion was presented by Albert Lee from CTBC Bank, who shared his bank's four strategies on how to design a client's journey changing the conditions of a market game. They are conducive to the growth of retail banking, combining good practices from both the mobile and physical worlds. According to Albert Lee, it is worth to:

- integrate digital channels and physical branches to provide the best omnichannel experience,

- create a possibility to locate the nearest physical branch in 3 simple steps in your mobile app,

- introduce biometric identification in branches to provide personalized services,

- enhance mobile app functionalities in order to become a mobile-first bank.

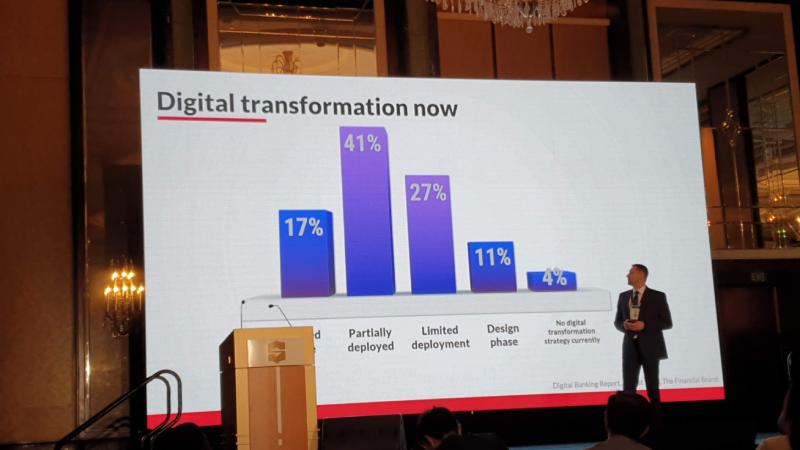

Tomasz Ampuła from Consdata presented the concept of digital transformation concerning sales processes, which made PKO Bank Polski help do its sales plan 4 times faster. He also, in turn, presented important aspects of digital sales transformation and the risks associated with them, together with effective and battle-proven ways to solve them. Michał Błaut from PKO Bank Polski, who presented together with Tomasz, explained how these concepts worked out in his bank.

It was so inspiring to hear how the Kenji bank follows the strategy of mobile-first or even mobile-only. The starting point for this bank was to jump over the stage of payment cards straight to the stage of mobile payments. In Poland, we remember how 30 years ago a similar situation took place when we, Poles, jumped over the cheque payments and went straight to card payments. That is why we are very much cheering for Charles Mudiwa and his bank.

Kazuya Sakakibara from Jibun Bank in Japan spoke about the mobility and digitalization of banking. He presented the changes taking place on the Japanese banking market, which are related, among others, to the upcoming Olympic Games 2020. It turns out that QR code payments are very popular in Japan and the government supports banks in popularizing contactless payments. At this point, it is also worth mentioning the relation to the European banking market. There are huge disproportions between the popularization of contactless payments in different countries - what is the norm for the Poles today is 20 times less popular just outside the western border of Poland, in Germany.

Stuart Smith from UOB Singapore shared another thought-provoking concept with the participants of the conference. Digitalization of banking or digital banks? The letters that make up these words are almost the same, yet the idea and meaning of these words is diametrically different. Digitalization of banking means to provide, among others, an omnichannel model that connects the worlds of e-banking and mobile banking with physical branches - for example, as presented by the aforementioned Albert Lee from CTBC Bank.

A digital bank is, on the other hand, only a virtual and mobile-oriented entity, with no branches, which is usually directed to a certain social group. On the example of "TMRW" implementation (read "tomorrow"), Stuart Smith showed how to combine mobility with simplicity, transparency, playability, and being helpful to customers rather than just sales-oriented.

Manohar Chadalavada from Standard Chartered Bank, mentioned earlier, also talked about how to do everything that other speakers talked about from the technological point of view. His experience shows that the application architecture based on micro-services is ideal. It simplifies implementation, helps support the modularity of solutions, improves customer experience, and reduces costs. Equally important are integrations with the use of API, which accelerate and reduce the costs of introducing changes and integration with external partners.

Ecosystems

All of the above-mentioned concepts concerned how the bank should be organized from the inside. However, during EFMA Asian Retail Banking Summit 2019 we also learned what model of cooperation with other economy players is attractive for both banks and other entities.

This concept is hidden in the word "ecosystem". It means creating value beyond just being a bank, and thus creating a new way to acquire new customers, as Suporn Sunthornrohit from Kasikornbank in Thailand, Nyoman Sugiri Yasa from Bank Rakyat Indonesia and Joel Kornreich, CEO of Alliance Bank Malaysia Berhad Group, told in their three presentations.

All the three speakers during their presentations shared positive experiences of creating ecosystems consisting of the banks in which they work in with other business entities. And so the participants of the congress could hear about how banks can derive tangible benefits from cooperation with small and medium-sized enterprises, e-commerce and tourist companies, or even with such industries as LPG gas suppliers or education.

Cooperation with Fintechs

So, on the one hand, we heard about how effective ecosystems of banks with other enterprises can be. But on the other, such a conference couldn't lack presentations on cooperation with Fintechs. For many speakers, this cooperation was emphasized as a "must have" for banks that want to have a chance to catch up with the leaders. According to the Manohar Chadalavada's from Standard Chartered Bank presentation's title, Fintechs provide banks with both data and ways to monetize them. Leandro Gimeno from Strands said that the only way to compete with banks now is to look for new solutions with Fintechs.

Fintechs can easily change the status quo of the market in which banks must find themselves. In cases such as the expansion of Revolut, we are not talking about Fintechs cooperating with banks, but about the fact that banks cannot remain passive. They need to change in order not lag behind like, for example, regular cabs facing the expansion of Uber.

Hyperpersonalization

A separate topic discussed at the EFMA Asian Retail Banking Summit 2019 was hyperpersonalization. Whatever banking model you adopt, whether you create ecosystems or not, whether you work with Fintechs or not, you must always put your customers in the spotlight.

In the age of ubiquitous digitalization, customers expect the same experience from banking as they expect from e-commerce. This is a real perspective, which Vipin Agrawal from CIMB Bank Berhad spoke about, among others. Moreover, references to the experience created by Amazon or Netflix were used by Anurag Mathur from HSBC Bank in Singapore. Now we all consider such references as classics.

So what should hyperpersonalization involve? As a bank, you should ensure that your offers are as personalized and tailored as much as possible - as mentioned during the conference that's not what your customers value - that's something they simply expect. Sometimes even going beyond the standard offerings, you should offer, for example, an alternative credit model with an optimal cost strategy from the customer's point of view. Hyperpersonalization is also triggers that can adjust Customer Journey uniquely to each individual customer.

However, all this will not be possible, as Royce Teo from DBS Bank Singapore stressed if banks do not implement technologies allowing for multidimensional collection and use of customer data in the first place. Secondly, if banks don't use customer data in accordance with the 'be PURE' principle, meaning being Purposeful, Unsurprising, Respectful, Explainable to your customers.

Challengers, Hyper-Personalization, Ecosystems and Fintechs: The Summary of EFMA Asian Retail Banking Summit 2019

The conference, which took place on 6 and 7 November in Singapore, was a really inspiring event for the banking world - not only Asian, but also global. The participants could listen not only to what and how so-called market challengers do, but also what can be done to catch up with leaders. I think that everyone brought out of Singapore a solid dose of knowledge and inspiration for changes in their local banking markets.

Read also the summaries: